What Is An Asset Depletion Mortgage And How Does It Work?

Some borrowers have a strong balance sheet and very little traditional income on paper. They may be retired, between business cycles, living off investments, or running a company in a way that keeps taxable income low. On a conventional mortgage application, that can create a frustrating result. The borrower may be financially strong, but the file looks weak.

That is where an asset depletion mortgage comes in. This type of loan is designed for borrowers who have meaningful liquid or near-liquid assets but do not show enough regular income through pay stubs, W-2s, or tax returns to qualify the traditional way.

For the right borrower, asset depletion can turn financial strength into mortgage qualifying power without forcing a liquidation event. Instead of asking only, “What do you earn each month from a job?” the lender asks a more useful question: “What level of income can reasonably be supported by the assets you already have?”

What An Asset Depletion Mortgage Actually Is

An asset depletion mortgage is a loan program that allows a lender to use eligible assets to create a qualifying income figure for mortgage approval.

You may also hear it described as an asset depletion loan, asset dissipation loan, or a form of asset-based mortgage. The basic idea is the same. Instead of relying only on paycheck-style income, the lender converts a portion of the borrower’s assets into a calculated monthly income amount for underwriting purposes.

This loan exists because many borrowers do not fit a standard income model. A retiree may have a large portfolio but modest monthly income. A self-employed borrower may have strong wealth and liquidity but low taxable income after deductions. A high-net-worth borrower may not want to sell investments simply to make the file look stronger.

In all of those cases, the issue is often not repayment ability. It is how the mortgage is being measured.

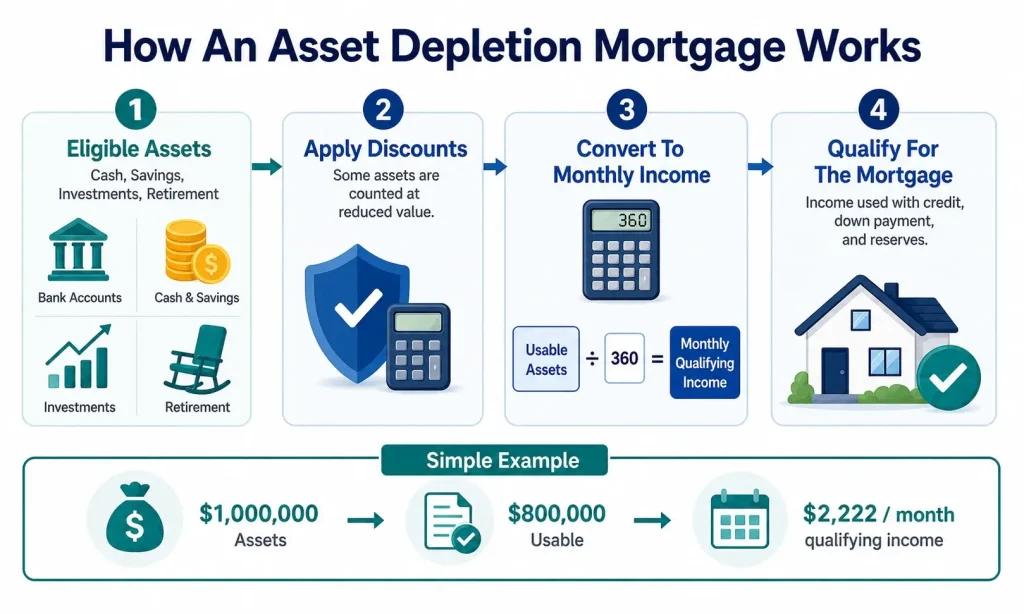

How An Asset Depletion Mortgage Works

The mechanics are fairly straightforward, even if the exact formula can vary by lender.

The lender starts by identifying eligible assets. These often include checking and savings accounts, money market funds, certificates of deposit, stocks, bonds, mutual funds, and in many cases retirement accounts. Not every asset is treated the same. Cash and cash-equivalent accounts are usually the easiest to count. Market-based assets and retirement accounts are often discounted to account for taxes, volatility, or access rules.

Once the eligible assets are adjusted, the lender converts them into a monthly qualifying income figure. A common method is to divide the adjusted asset total by 360 months, which mirrors a 30-year mortgage term. Some lenders use different methods, but the purpose is the same: to estimate what level of monthly income your assets can reasonably support over time.

That resulting monthly figure may then be used on its own or combined with other income sources to qualify the borrower.

What Assets Usually Count

Eligible assets typically include liquid and investment accounts that can be documented and verified. That often means checking accounts, savings accounts, money market accounts, certificates of deposit, stocks, bonds, and mutual funds.

Retirement accounts may also count, but they are often treated more carefully. Depending on the borrower’s age, accessibility, and the lender’s guidelines, only a portion of those funds may be counted. This is because lenders want to account for penalties, taxes, and limits on immediate access.

Real estate equity usually is not treated the same way unless it is tied to another structured program. Asset depletion is generally focused on financial assets that can be converted into a reliable qualifying figure.

The important point is that not all asset value becomes usable qualifying income. Lenders want a conservative approach, not an inflated one.

How The Calculation Usually Works

A simple example makes the structure easier to understand.

Suppose a borrower has $1,200,000 in eligible assets. After the lender applies any required discounts to investment or retirement accounts, the usable amount comes out to $900,000. If that number is divided by 360 months, the borrower may receive a qualifying income figure of $2,500 per month.

That monthly figure may be enough to support the mortgage on its own, or it may be combined with other income such as Social Security, pension income, rental income, or part-time work.

The exact math varies by lender, but the principle remains consistent. Asset depletion converts stored wealth into an underwriting-friendly monthly income amount without requiring the borrower to immediately sell everything to qualify.

Who Asset Depletion Mortgages Are Best For

This loan is best for borrowers whose real financial strength is tied more to assets than to traditional income documentation.

Retirees are a natural fit. Many have substantial savings, investment accounts, or retirement assets but may no longer receive enough regular employment income to satisfy a conventional lender.

Self-employed borrowers can also be strong candidates. A business owner may have excellent liquidity and a solid overall balance sheet but show low taxable income because of write-offs, depreciation, or business deductions. In those situations, a conventional underwriter may see low income, while an asset depletion lender may see a financially strong borrower.

High-net-worth borrowers also benefit from this structure. Some do not want to liquidate investments just to create more visible income. Others may be between major income events, relying on asset strength while maintaining a broader financial strategy.

In each case, the core issue is the same: traditional income documents do not tell the full story.

What Still Matters Beyond Assets

Asset depletion is not a free pass around underwriting. It is a different underwriting approach, but it is still underwriting.

Credit score still matters. So does the size of the down payment, the overall loan-to-value ratio, reserves, liabilities, and the general strength of the file. A borrower with meaningful assets but weak credit or an overstretched balance sheet may still run into trouble.

Down payment expectations are often stronger than what some conventional borrowers may expect. Many asset depletion scenarios work best when the borrower brings meaningful equity into the transaction. The lender wants to see not only assets, but a conservative overall risk profile.

Reserves also matter because they reinforce the borrower’s ability to manage the property and mortgage comfortably after closing. A lender wants to know the asset story is not thin, temporary, or overly strained by the new loan.

In other words, assets matter a lot, but they are still only one piece of the approval picture.

Do You Have To Liquidate Assets To Qualify?

Usually, no.

That is one of the biggest misconceptions around this type of loan. Asset depletion generally allows the lender to use your assets for qualification without requiring you to sell them all upfront just to manufacture income.

That does not mean every dollar stays untouched forever. It means the program is designed to recognize the borrower’s financial strength without forcing unnecessary liquidation as the only path to approval.

For many borrowers, that is the real appeal. They can preserve their broader investment strategy while still qualifying for a mortgage based on the strength of what they already own.

Asset Depletion Mortgage Vs. Bank Statement Loan

This is one of the most important comparisons because the right loan depends on what actually makes the file strong.

An asset depletion mortgage is usually the better fit when assets are the strongest part of the borrower’s profile. If the borrower has meaningful liquid funds, investments, or retirement assets, but limited traditional income, asset depletion may be the cleaner solution.

A bank statement loan may be the better fit when the borrower’s actual monthly cash flow is strong, but their tax returns understate it. That often happens with self-employed borrowers whose deposits show a stronger and more consistent income story than their tax returns do.

This distinction matters because many borrowers technically qualify for more than one Non-QM path, but only one may be the best strategic fit. The goal is not to force every borrower into asset depletion. The goal is to use the structure that aligns with the borrower’s real financial strengths.

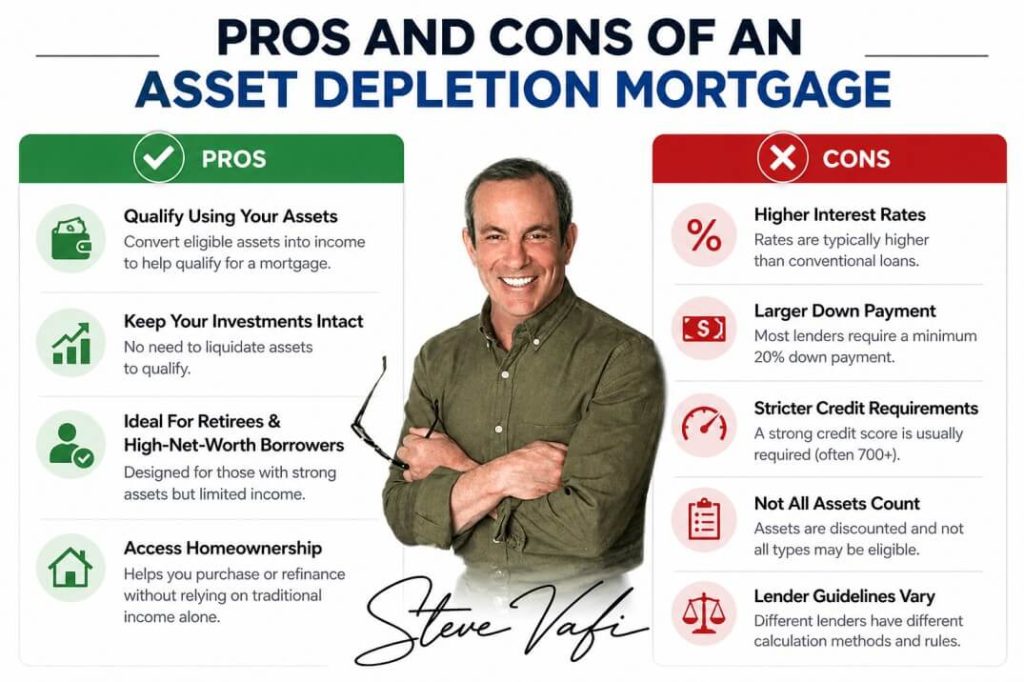

Pros And Cons Of An Asset Depletion Mortgage

The biggest benefit is flexibility. A borrower who would otherwise look weak in a conventional file can become much stronger when the lender accounts for verified assets.

This can help retirees, self-employed borrowers, and high-net-worth clients qualify without relying on traditional paycheck-style income. It also allows borrowers to keep investments intact rather than restructuring their financial life just to satisfy a standard underwriting formula.

The tradeoffs are real, though. Asset Depletion Loans may carry higher rates or stricter terms than the most competitive conventional loans in some cases. Down payment expectations can also be higher. And not every asset counts equally, which means the borrower may not be able to use the full face value of their portfolio in the way they expect.

There is also the simple fact that lender calculations vary. Two lenders may not treat the same borrower exactly the same way. That is why structure and lender fit matter so much.

Why This Matters For Borrowers Who Were Told No

One of the strongest reasons to understand asset depletion is that it often applies after a borrower has already been told they do not qualify.

That denial can be misleading. The borrower may not have an income problem. They may have a loan-structure problem.

A traditional lender may look at the file and see low verifiable monthly income. An asset depletion lender may look at the same file and see substantial qualifying power based on liquid assets and overall financial strength.

That does not mean every denied borrower is a fit. But it does mean a denial should not always be treated as the final answer. Sometimes it is simply the result of using the wrong mortgage framework.

Why Choose ABO Capital

ABO Capital helps borrowers find mortgage solutions when conventional lending does not reflect their real financial picture. That includes self-employed borrowers, real estate investors, and high-asset clients who need a more strategic approach to qualifying. Instead of forcing every file into a standard model, ABO Capital focuses on matching the right loan structure to the borrower’s income, assets, and long-term goals.

How ABO Capital Looks At Asset Depletion Strategically

Asset depletion is not just a formula. It is a loan strategy.

For the right borrower, it can solve a very specific problem: strong assets, weak conventional income. But it is not always the best answer. Some borrowers are better served by bank statement loans. Others by DSCR. Others may still qualify conventionally with the right planning.

That is why the best approach is not product-first. It is borrower-first. You start with the real financial picture, then decide which structure best supports it.

For asset-rich borrowers, that can mean unlocking a mortgage path that a traditional lender never properly evaluated.

Frequently Asked Questions

What Is An Asset Depletion Mortgage?

It is a mortgage that allows a lender to use eligible assets to create a qualifying income figure for approval.

How Does An Asset Depletion Mortgage Work?

The lender identifies eligible assets, applies any required discounts, and converts the usable amount into a monthly income figure using an underwriting formula.

What Assets Count For Asset Depletion?

Checking, savings, money market accounts, CDs, stocks, bonds, mutual funds, and in many cases retirement accounts may count.

Do You Have To Liquidate Assets To Qualify?

Usually no. In many cases, the assets are used for qualification without requiring immediate liquidation.

Who Qualifies For An Asset Depletion Loan?

Common candidates include retirees, self-employed borrowers with low taxable income, and high-net-worth borrowers with substantial liquid or investment assets.

What Else Matters Besides Assets?

Credit score, down payment, reserves, overall liabilities, and general file strength still matter.

Is Asset Depletion Better Than A Bank Statement Loan?

It depends on what makes the borrower strongest. If assets are the main strength, asset depletion may be the better fit. If monthly business cash flow is stronger, a bank statement loan may work better.

Is An Asset Depletion Mortgage A Non-QM Loan?

In many cases, yes. It is often positioned as a Non-QM solution for borrowers who do not fit conventional income documentation guidelines.